Our AI-driven technology paired with industry experts provides streamlined compliance processes and lowers risk.

Intelligent Tax Compliance for a Strategic Business

Transfer Pricing

R&D Tax Credit

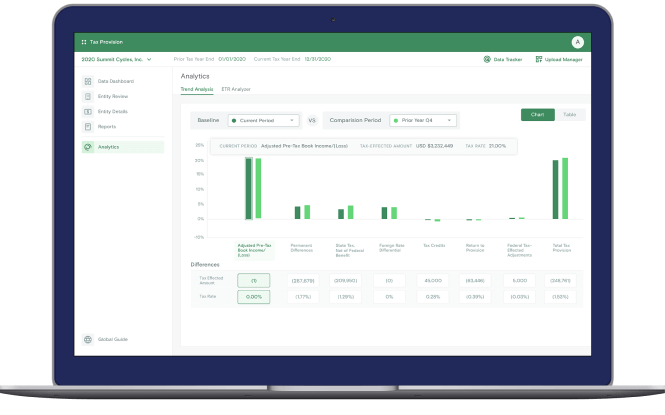

Tax Provision

Transfer Pricing

Exactera Transfer Pricing

Protect Yourself From Penalties

Exactera Transfer Pricing is a complete solution delivered by transfer pricing experts and powered by AI. It is the intelligent approach to transfer pricing and exemplifies the intersection of human and machine intelligence. One centralized solution for localized compliance with reduced risk at a lower cost.

The R&D tax credit is the largest annual tax credit available to U.S. companies and applying for the credit is easier and more affordable than you think, thanks to our R&D tax credit software-based services. Ensure you are getting the maximum R&D tax credit you are entitled to and streamline the process with Exactera.

Exactera Tax Provision bypasses the usual Excel roadblocks—broken links, data-entry errors, workbooks that don’t flow seamlessly—and helps automate the book-to-tax process, computes complex calculations swiftly and accurately, and produces audit-ready standard reports, including the a detailed tax account roll-forward (TARF). Our customers reduce the time to complete their tax provision by up to 65%, saving weeks of time.

Managing Transfer Pricing Compliance in a Post-BEPS World

With entities in the U.S., Brazil, Puerto Rico, the U.K., and Australia, Red Ventures is under the watchful eye of some of the most aggressive tax authorities in the world. ”The majority of Red Ventures’ transactions involve intellectual property and intercompany services—two of the most highly scrutinized types of transfer pricing transactions,” said Ray Salort, VP of Tax, Red Ventures. “We absolutely had to have consistent, detailed documentation across all our jurisdictions, but we didn’t have this available in any efficient or centralized manner.”

Originally, Red Ventures tried a couple of different methods to outsource its transfer pricing documentation, including hiring a Big Four accounting firm as well as hiring various local consultants. But they found the process in each case was laboriously manual and haphazard, producing reports that were not always consistent from jurisdiction to jurisdiction. Turnaround time for reporting requests was also lengthy.

Red Ventures needed to streamline and centralize its transfer pricing processes, produce more detailed, consistent documentation quickly and efficiently across all jurisdictions, and organize reports so they’d have studies to refer to from year to year.

Transforming Compliance into a Streamlined Operation Red Ventures has intercompany transactions all over the world, which means transfer pricing documentation has to meet unique local regulations in various jurisdictions. The company decided to look for a solutions provider that could accommodate their reporting needs across all their jurisdictions with the efficiency, control, and accuracy they required. Exactera’s transfer pricing solution was chosen because it enabled Red Ventures to centralize how they were able to generate reports and construct a consistent approach to reporting for each jurisdiction where they operated. Red Ventures was able to home in on their intercompany transactions, identify new ones, and produce robust documentation across the board, with equal or better accuracy, and more cost-effectively compared to other methods.

Getting More For Less

“Aside from the capabilities of the solution, another deciding factor for us in choosing Exactera was transparent, competitive pricing,” said Salort “Our tax department could now generate more detailed reports, at a lower cost than what we paid traditional consultants.” CrossBorder Solutions also made benchmarking searches more cost-effective and faster by leveraging prior years’ benchmarks instead of starting from scratch.

The Value of a Highly Collaborative Approach

Exactera’s expertise made the process of transitioning from traditional outsourcing to software easier and more simplified for Red Ventures. Exactera made onboarding easy with straightforward questions, and since deliverables were on schedule, it left enough time for our tax team to review and make strategic decisions. “We had the same level of expertise as we did at the Big Four—if not better,” said Salort. Exactera’s consultative approach to the partnership with Red Ventures meant that there was a high degree of collaboration, as well as responsive and professional communication. Red Ventures could now proactively approach its transfer pricing, which helped the tax department deliver greater business value. Exactera’s team of economists provided consulting and education on how tax authorities view transfer pricing documentation and how to think about related-party arrangements. This allowed Red Ventures’ tax professionals to identify intercompany transactions, value drivers, and intellectual property resulting from those transactions.

Exactera was able to help Red Ventures identify areas of potential risk and proactively address them. One example was how Red Ventures, could identify service transactions that generated intellectual property in foreign jurisdictions and could create legal licensing agreements and properly allocate profits. The solution also took the guesswork out of benchmarking searches by producing reliable comparable data, reducing the risk of audits and adjustments, and enabling Red Ventures to maintain a better global tax position.

Integrating Tax into the Business Strategy, Delivering Business Value With Exactera

Red Ventures could tackle more than just transfer pricing documentation—they’ve been able to incorporate tax into part of the company’s business plan. “Working with Exactera connected us with the business more,” says Salort. “The business folks know exactly what we’re doing, and they understand the importance of it.”

By looking at the company holistically, Red Ventures was able to identify and understand key value drivers and how to allocate profits based on that value-add. Understanding how key functions make up the value chain also enables the company to produce more detailed documentation. Red Ventures has been able to apply a single, organic process to the entire group, base transfer prices on reliable comparable data, and allocate profits in advantageous jurisdictions, which saves money and adds to the company’s bottom line. “We have saved millions of dollars in taxes thanks to Exactera,” says Salort. “We’re extremely confident that we have well-documented, accurate reports and that we’re in a stronger global tax position thanks to our work with Exactera.”

Red Ventures

Ray Salort, VP, Tax

Exactera's technology exceeds its competitors and offers a better product at a better price.

With only a four-person tax department and global transfer pricing issues, Dyno Nobel is no stranger to transfer pricing compliance consultants. But why does outsourcing always seem to mean that you pay exorbitant fees for services—and then work on their terms? It was time for a change. The company enlisted Exactera to produce efficient reports, provide expertise, and free up the lean tax department to focus on other priorities. The result? More coverage, less work, and fewer costs.

Dyno Nobel

Milan Crane, Tax Director/Risk Manager

67%transfer pricing cost reduction

It reduced a lot of stress and gave me back so much time to be more efficient in other areas.

Roseburg Forest Products needed to find an alternative approach to complex, messy Excel spreadsheets and manual processes. They needed to maintain ownership of the data but wanted to explore a more automated, software-based approach. Choosing Exactera Tax Provision, the team was able to achieve greater efficiency, ensure calculation accuracy, and shaved weeks off their provision process timeframe.

Roseburg Forest Products

Andrea Evans, Tax Manager

Exactera prepared thorough documentation and saved time and money.

When a company experiences growth, it’s great for everyone—except maybe the tax department. And if you happen to be a one-person tax department then a business boom can be even more daunting—which is exactly the situation Jaggaer’s Global Director of Tax Angela Griffin found herself in.

Before 2017, Jaggaer was a relatively simple U.S. company. But over the last five years, the software giant has spilled into Italy, Austria, Australia, Canada, Dubai, France, Germany, Italy, Saudi Arabia, Serbia, Mexico, Netherlands, Singapore, Spain, and UK, to name just a few countries. As the group grew more intricate, it bred a wild new maze of transfer pricing arrangements. Each new entity had its own historical related-party transactions, and now under one larger umbrella, the sister companies were forging new ones–but with eyes on efficiency and quality-control, not compliance.

For Griffin this meant a huge responsibility rest on her shoulders alone: She had to track down each and every intercompany arrangement throughout the conglomerate and make sure they were not only documented but that they were detailed enough to stand up in a post-BEPS world. The Big Four might seem like an obvious answer but like at most companies, the budget was tight.

Griffin found herself in a race against the clock. Many transactions hadn’t been documented at all and she found a host of arrangements that hadn’t even been identified as transfer pricing transactions. “I discovered we had cross charges that we didn’t consider in our IP transfer pricing planning. We had intercompany loan arrangements, various service type transactions ranging from customer service, implementation, management type services and then we realized we had other intercompany service transactions not previously identified in any agreement,” she says.

COVID remote working combined with new mergers and acquisitions also created a migrating workforce, especially in Europe. Teams that were previously in Italy were transitioned to Serbia and were performing services from Serbia. Teams from France had relocated to the Netherlands, and so on. As new head count was added the Serbia service center multiplied and grew exponentially. However, outside the tax department, executives were oblivious that such transfers would require new transfer pricing documentation. Griffin had to educate executives and teammates about the tax implications of functions moving through the supply chain and streamline the group’s approach to transfer pricing from the ground up. And she had to work fast.

Building a Team

The sheer volume of reports that Jaggaer had to produce was hardly a job for a one-person tax department. Jaggaer needed an efficient, knowledgeable transfer pricing team and found it at Exactera. “They are transfer pricing experts and I loved their breadth of knowledge,” says Griffin. The cost was also appealing. Instead of exorbitant hourly rates, Exactera charged a lump sum for all of Jaggaer’s transfer pricing—even for new arrangements that were identified along the way–so there were no hidden fees. “When we needed additional benchmarking for new transactions Exactera was able to help provide at no additional cost.” Best of all, Griffin had an invested team in place. “Exactera made efforts to know our company. The economists talked through our transfer pricing planning and questioned it instead of just accepting what we gave them. It was almost like a second review.”

Compliance in a Hurry

The need to document so many intercompany arrangements accurately on unique, tight deadlines called for automation. Exactera’s software is able to streamline the process and get the job done quickly—transactions that require fresh benchmarking searches can be completed in seconds. Their unique software can identify and report documentation needed for compliance quickly, and Exactera’s economic experts could advise on little-known country-specific preferences. Jaggaer chose to utilize the Exactera team for outsourced benchmarking and compliance documentation versus hands on and in house usage of their software to ensure transactions are covered from every angle.

“We needed to ensure that the company has accurate, defendable positions that are documented well in all countries where we had operations—and we needed a comprehensive plan for the whole company,” Griffin says.

Building Bridges

Deadlines and language barriers were also tricky. Each country had its own deadline for documentation submission or completion, there were secret preferences regarding transfer pricing methods, and tax terminology meant one thing in country X and another in country Y. “The language barrier has hindered communication and understanding of proper categorization, especially for the various types of intercompany services. That’s how we get incorrect markups that are not apparent until year end,” says Griffin, who discovered having someone on the inside is very helpful. “We’ve utilized Exactera’s Italian specialists on formatting of the reports in Italy. When we have unique transactions,E it helps to have someone who speaks Italian to discuss the local requirements and comfort our local employees on the accuracy of our reporting.”

Education and Efficiency

Griffin literally found herself working in uncharted territories—the company’s operations were growing in many unfamiliar jurisdictions. She also had to document transactions involving IP and intercompany services—two of the most highly scrutinized transactions by tax authorities. The pressure was on.

Exactera’s economic experts were able to advise on complex transactions and identify those that would likely be under the microscope. Meanwhile, Griffin was able to advance her own in-depth knowledge and earn CPE credits by taking Exactera’s Transfer Pricing University. Other staff members–like Jaggaer’s controller—joined her and benefited as well.

“It’s been a huge learning experience,” she says.

Certain transactions required fresh benchmarking searches, and Griffin, usually a solo act, had a team with which to collaborate. “When we’ve had issues that required benchmarking, we were able to ask a lot of questions without incurring additional fees.” Together, the team decided on “agreed-upon terminology,” a vocabulary lesson she was able to impart to Jaggaer’s financial controllers to ensure the company was always on the same page.

Exactera reached out to Jaggaer for information and then prepared documentation for the entire group. Griffin noted early conversations about the company and each transaction are key. “They prepared thorough documentation. Each report describes the parent’s relationship with the entity and also includes a visual presentation, which is helpful,” says Griffin. “Exactera loaded them onto the portal, and we just had to review them.”

Confident Compliance

Exactera was able to help identify and produce documentation for the continuously growing Jaggaer, so now, the company’s transfer pricing is in compliance all over the world. Plus, Jaggaer has a process in place that streamlines compliance and makes it a slick operation throughout the group.

Griffin feels much better about the company’s transfer pricing position. “I feel more confident now that our transfer pricing documentation has been prepared,” she says. “Exactera has saved me lots of time. I didn’t have the experience or time to create these documents myself, especially in such a short timeframe. Exactera helped us be compliant. Given our sudden growth, we wouldn’t have been able to be compliant without tax technology.”

Had she gone with traditional consultants, the cost would have been exorbitant. As Griffin said, “Exactera has given us a lot of bang for our buck.”

67 % transfer pricing cost reduction

67 % transfer pricing cost reduction